Many savers and investors earn interest from bank accounts or investments, but confusion often starts when tax season arrives. People regularly ask, how much tax do you pay on interest income, and the answer depends on where that income comes from and your overall earnings. Interest income may look small on paper, yet taxes can reduce it if you are not prepared. This matters for everyday savers, retirees relying on fixed income, and investors holding bonds or cash-based assets. Understanding the rules early helps you avoid surprises, penalties, or missed reporting. In this guide, you will learn how interest income works, whether it is taxable, how federal and state tax rates apply, and how to report it correctly. By the end, you will clearly know how interest income fits into your tax return and what actions can reduce your tax bill legally.

2. What Is Interest Income?

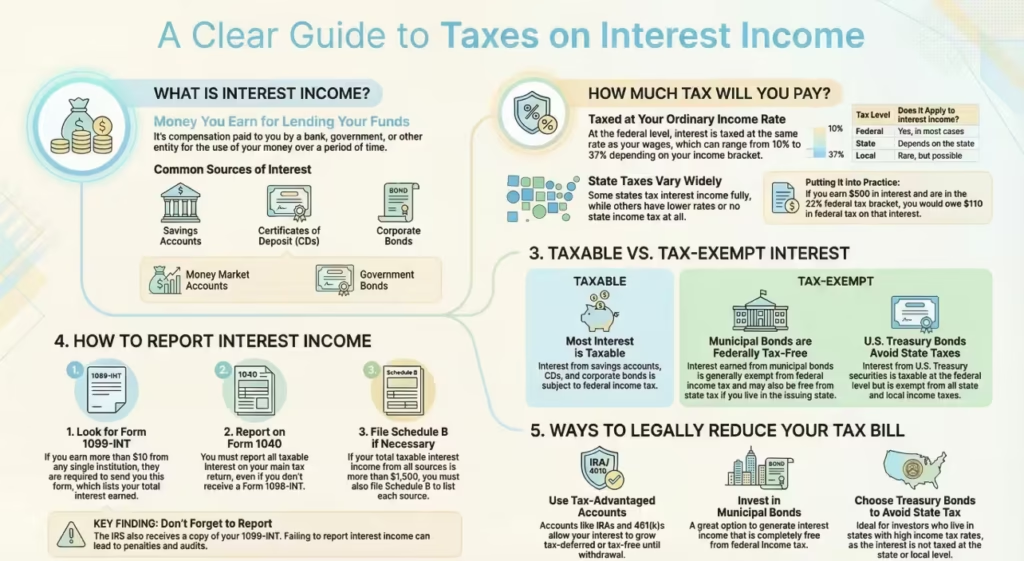

Interest income is the money you earn for allowing a bank, government, or institution to use your funds for a period of time. It is usually paid as a percentage of your deposited or invested amount. For most people, interest income comes from common financial products used for saving or stability rather than growth. Typical sources include savings accounts, certificates of deposit (CDs), money market accounts, bonds, and even personal loans you issue to others. The basic calculation of interest income follows a simple formula: principal multiplied by the interest rate and the time the money is held. For example, depositing $10,000 at a 4% annual rate earns $400 in one year. Even though it feels passive, the IRS treats this income similarly to wages in many cases, which is why understanding its tax treatment is important.

3. Is Interest Income Taxable?

A common question is, is interest income taxable in the United States? In most situations, the answer is yes. The majority of interest income is taxed as ordinary income at the federal level. This includes compund interest earned from savings accounts, CDs, corporate bonds, and money market funds. However, there are important exceptions that can reduce or remove the tax burden. Interest from municipal bonds is often exempt from federal income tax and may also be free from state tax if you live in the issuing state. In addition, interest earned on U.S. Treasury bonds is taxable federally but exempt from state and local taxes. These distinctions matter because they can change how much tax you owe on interest earned, especially for high-income earners or retirees holding large bond portfolios.

4. How Much Tax Do You Pay on Interest Income?

Federal Tax

At the federal level, interest income is taxed at your ordinary income tax rate, which is the same rate applied to wages or self-employment income. Current tax brackets range from 10% to 37%, depending on your total taxable income for the year. The U.S. tax system uses marginal rates, meaning different portions of your income are taxed at different rates, while your effective rate reflects the average tax paid overall. Interest income stacks on top of your other income and can push part of your earnings into a higher bracket.

State & Local Tax

State taxation varies widely. Some states tax interest income fully, others partially, and several states charge no income tax at all. This difference can strongly affect total interest income tax rates depending on where you live.

| Tax Level | Applies to Interest Income? |

|---|---|

| Federal | Yes, in most cases |

| State | Depends on the state |

| Local | Rare, but possible |

5. How To Report and Pay Tax on Interest Income

Reporting interest income correctly is required by the Internal Revenue Service. If you earn more than $10 in interest from a financial institution, you will usually receive Form 1099-INT by early February. This form shows the total interest you earned during the year and is also reported directly to the IRS. All taxable interest must be included on Form 1040, even if a form is not issued. If your total taxable interest exceeds $1,500, Schedule B is required to list each source. Many taxpayers use an Interset loan calculator or compound interest tracking tools to estimate earnings accurately before filing. Failing to report interest income can result in penalties or audits, so keeping year-round records and reviewing bank statements helps ensure accurate and stress-free tax filing.

6. Examples

Examples help clarify how interest income tax works in practice. Suppose you earn $500 in interest from a savings account and fall into the 22% federal tax bracket. In this case, you would owe $110 in federal income tax on that interest alone. If your state has a 5% income tax, that adds another $25, bringing the total tax to $135.

Here is a simple breakdown:

| Interest Earned | Federal Rate | Federal Tax |

|---|---|---|

| $500 | 22% | $110 |

If the same $500 came from a tax-exempt municipal bond, the federal tax could be zero. These examples show why the source of interest income matters just as much as the amount earned.

7. Special Situations & Exceptions

Certain situations change how interest income is taxed. Municipal bonds often provide tax-free interest at the federal level, while corporate bonds do not. Nonresident aliens usually face a flat 30% federal tax rate on U.S.-source interest income unless a tax treaty lowers that rate. High-yield savings accounts also generate taxable interest, even though the earnings are paid monthly and may feel small individually. Some foreign bank accounts require additional reporting under international tax rules. Retirement accounts such as traditional IRAs can delay taxes on interest income until withdrawals occur. Each of these cases follows specific rules, so understanding where your interest income comes from helps avoid errors and missed opportunities for tax savings.

8. Ways to Reduce Tax on Interest Income

While interest income is often taxable, there are legal ways to reduce how much tax you pay. Using tax-advantaged accounts like IRAs or 401(k)s allows interest to grow without immediate taxation. Investing in municipal bonds can reduce or eliminate federal tax on interest earned. Timing interest income also matters; spreading earnings across years may keep you in a lower tax bracket. Some savers choose Treasury bonds to avoid state taxes altogether. These strategies do not eliminate tax obligations but can lower their impact over time. Planning ahead rather than reacting during tax season often leads to better outcomes, especially for retirees or high-income savers relying heavily on interest income.

9. FAQs

Do I pay tax on all interest income?

Most interest income is taxable, but municipal bond interest and some government securities receive special treatment.

Does my bank send a tax form?

Yes, banks usually send Form 1099-INT if you earn more than $10 in interest.

What happens if I don’t report interest?

Unreported interest can result in penalties, interest charges, or audits.

Is interest income taxed differently than dividends?

Yes. Interest income is taxed as ordinary income, while qualified dividends may receive lower tax rates.

10. Conclusion

So, how much tax do you pay on interest income? The answer depends on your income level, where you live, and the source of the interest. Most interest income is taxed at ordinary federal income tax rates, with state taxes adding another layer in many cases. Exceptions such as municipal bonds and Treasury securities can reduce that burden. Proper reporting using IRS forms is required, even for small amounts. With smart planning, it is possible to lower taxes through account selection and investment choices. Understanding these rules helps savers, investors, and retirees protect their earnings. If your situation involves large interest income or special cases, speaking with a qualified tax professional can provide clarity and peace of mind.