How to Use This Capital Gains Tax Calculator (Step-by-Step Guide)

Using a capital gains tax calculator correctly is just as important as having access to one. This section acts as a bridge between user experience and clear understanding, ensuring that the numbers produced reflect real-world tax rules. Each input field plays a specific role in determining your estimated tax outcome, and small errors can lead to misleading results. This calculator is designed to mirror U.S. federal tax logic, but it depends on accurate information from the user. By following each step carefully, investors can gain a realistic picture of how much tax they may owe and how their decisions affect after-tax returns. Whether you are selling stocks, cryptocurrency, or another taxable asset, understanding how to enter data and interpret results allows you to plan ahead rather than react later during tax filing season.

Entering Purchase and Sale Prices Correctly

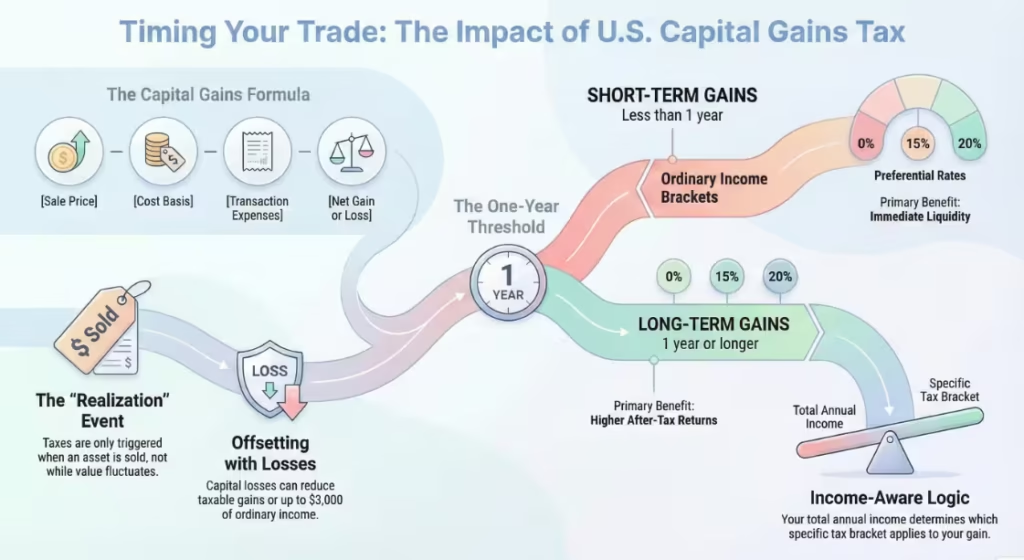

Purchase and sale prices form the foundation of any capital gains calculation. The purchase price, often called the cost basis, should reflect the actual amount paid for the asset, including any initial fees or commissions. If the asset was acquired through multiple purchases, the correct cost basis may require averaging or lot selection. The sale price should represent the gross amount received before taxes, not the amount deposited after deductions. Adjustments such as brokerage fees, exchange fees, or commissions should be entered separately when the calculator allows for expenses. Accurate entry of these values ensures the net gain or loss reflects reality. Even small inaccuracies can significantly affect tax estimates, especially for high-value transactions or frequent trading activity.

Selecting the Correct Holding Period

The holding period determines whether a gain is classified as short-term or long-term, which directly impacts the tax rate applied. Under IRS rules, an asset is considered long-term only if it is held for more than one full year. Selling even one day earlier places the gain in the short-term category. A common mistake is assuming that holding an asset during parts of two calendar years qualifies as long-term, which is incorrect. The holding period begins the day after acquisition and ends on the day of sale. Selecting the correct option in the calculator ensures the appropriate tax structure is applied. This single input often makes the largest difference in the final tax estimate.

Filing Status and Income Inputs Explained

Filing status and annual income determine which tax brackets apply to both short-term and long-term gains. Filing status options such as single, married filing jointly, married filing separately, or head of household each have different income thresholds. Income input should reflect total taxable income for the year, not just investment income. This matters because capital gains are layered on top of existing income when determining tax rates. Many users underestimate the impact of income on capital gains tax, assuming a fixed rate applies. Accurate income and filing status inputs allow the calculator to apply the correct marginal or preferential rate, producing a more reliable estimate.

Understanding the Results

The results section summarizes how each input affects your estimated tax outcome. Capital gain or loss shows the net profit after expenses. Tax owed reflects the estimated federal tax due on that gain. The effective tax rate explains the percentage of the gain paid in tax, which may differ from marginal rates. Net proceeds after tax show what remains after taxes and expenses. The comparison chart highlights the difference between short-term and long-term tax outcomes, helping users visualize potential savings. Together, these results provide clarity, allowing users to assess whether selling now or later aligns better with their financial goals.

Capital Gains Tax Calculation Examples (Real-World Scenarios)

Examples help translate tax rules into practical understanding. By walking through realistic situations, users can see how capital gains tax works across different assets and income levels. These scenarios illustrate how holding periods, income brackets, and asset types influence tax outcomes. They also reinforce why planning matters before selling an investment. Each example applies the same calculation logic but produces different results based on individual circumstances. This approach builds trust by showing how theory applies in practice, rather than relying on abstract explanations alone.

Example 1: Selling Stocks at a Profit

Consider an investor who buys shares of a publicly traded company for $10,000 and sells them later for $15,000. After accounting for $200 in brokerage fees, the net gain is $4,800. If the shares were held for six months, the gain is short-term and taxed at ordinary income rates. If held for over a year, the gain qualifies for long-term rates, which are often lower. For many taxpayers, the difference can amount to hundreds or thousands of dollars. This example shows how the same profit leads to different tax outcomes based solely on timing, reinforcing the importance of holding period awareness.

Example 2: Cryptocurrency Capital Gains

Cryptocurrency transactions follow the same capital gains rules as other taxable assets, despite price volatility and trading frequency. Suppose an individual buys digital currency for $5,000 and later sells it for $12,000. The $7,000 gain is taxable once the asset is sold. If the holding period is under one year, the gain is short-term and taxed as ordinary income. If held longer, preferential long-term rates may apply. Volatility increases the likelihood of gains and losses within short periods, making accurate tracking essential. This example highlights that while the asset class differs, the tax logic remains consistent.

Example 3: High-Income Investor Scenario

A high-income taxpayer selling an investment may face additional considerations beyond standard capital gains tax. Suppose an individual with significant annual income realizes a large long-term gain. While the base long-term rate may be 20%, an additional 3.8% Net Investment Income Tax may apply. This can raise the total effective tax rate. Many confuse marginal and effective rates, assuming the entire gain is taxed at the highest rate. In reality, different portions may be taxed differently. This example clarifies how income level influences total tax liability and why calculators must consider income thresholds.

Strategies to Reduce or Optimize Capital Gains Tax Legally

Reducing capital gains tax involves planning, timing, and understanding how tax rules interact with investment decisions. While no calculator replaces professional advice, understanding common strategies helps investors make informed choices. Legal optimization focuses on aligning actions with existing tax rules rather than avoiding taxes improperly. Small adjustments, such as timing a sale or offsetting gains, can significantly improve after-tax outcomes over time. These strategies are widely used and supported by tax regulations.

Timing Asset Sales to Qualify for Long-Term Rates

Holding discipline is one of the simplest ways to reduce capital gains tax. Waiting until an asset qualifies for long-term treatment often results in lower tax rates. This approach requires patience and awareness of holding periods, especially near the one-year mark. Investors who plan sales in advance can avoid unnecessary short-term taxation. Timing decisions should consider both market conditions and tax impact. Understanding this balance helps preserve more value from successful investments.

Tax-Loss Harvesting Explained

Tax-loss harvesting involves selling assets at a loss to offset taxable gains. Losses can reduce or eliminate capital gains tax in the same year and may also offset a limited amount of ordinary income. Excess losses can be carried forward to future years. One important rule to understand is the wash sale rule, which prevents claiming a loss if the same or similar asset is repurchased within a short window. Used properly, tax-loss harvesting can smooth tax outcomes across years and improve long-term efficiency.

Using Tax-Advantaged Accounts

Tax-advantaged accounts such as IRAs and 401(k)s treat gains differently than taxable accounts. Within these accounts, capital gains are not taxed when assets are sold. Instead, taxes are deferred or handled under separate rules during withdrawals. This structure allows investments to grow without annual capital gains tax. Understanding how these accounts work helps investors decide where to place assets and how to structure long-term strategies.

Income Management and Threshold Awareness

Staying within lower income thresholds can reduce capital gains tax exposure, especially for long-term gains that may qualify for a 0% rate. Income management involves planning sales across years, coordinating with other income sources, and understanding filing status thresholds. Year-by-year planning can prevent sudden spikes in taxable income. Awareness of thresholds helps investors avoid unnecessary tax increases and supports more predictable financial outcomes.

Limitations of Capital Gains Tax Calculators

While calculators are useful planning tools, they have limits that users should understand. Most calculators focus on federal taxes and do not include state capital gains tax, which varies by location. Additional taxes such as the Net Investment Income Tax or Alternative Minimum Tax may not be fully reflected. Certain assets follow special rules, and real estate transactions may involve exclusions not covered by standard calculators. Estimates are not the same as filed tax returns, which require official forms and full documentation. Transparency about these limits builds trust and encourages responsible use.

Frequently Asked Questions About Capital Gains Tax

How accurate is this capital gains tax calculator?

This capital gains tax calculator provides a reliable estimate based on current U.S. federal tax rules and the information you enter. Accuracy depends on entering correct purchase prices, sale prices, income, filing status, and holding period. The calculator does not replace official tax forms or professional advice, but it is very useful for planning and understanding potential tax outcomes before you sell an asset.

Does this calculator include state capital gains tax?

No, this calculator estimates federal capital gains tax only. State capital gains taxes vary widely by location, and some states do not tax capital gains at all, while others tax them as ordinary income. Because state rules differ and change frequently, they are not included in this calculation and should be reviewed separately.

Do I pay capital gains tax if I reinvest the money?

Yes, reinvesting the proceeds does not eliminate capital gains tax. Capital gains tax is triggered when you sell an asset at a profit, regardless of how the money is used afterward. Even if you immediately reinvest the funds into another investment, the original sale is still taxable under federal tax rules.

How are crypto capital gains taxed?

Cryptocurrency is taxed using the same capital gains rules as stocks and other investments. If you sell, trade, or spend cryptocurrency at a profit, the gain is taxable. Assets held for less than one year are taxed as short-term gains, while assets held longer than one year may qualify for lower long-term capital gains tax rates, depending on income.

What happens if I have multiple transactions?

If you have multiple transactions during the year, all capital gains and losses are combined. Gains from profitable sales are offset by losses from unprofitable sales to determine your net capital gain or loss. This net amount is what ultimately affects your tax calculation for the year.

Is capital gains tax calculated per transaction or annually?

Capital gains occur on each individual transaction, but taxes are calculated on an annual basis. At the end of the tax year, all gains and losses are added together along with your income to determine how much capital gains tax you owe. This is why year-end planning and accurate recordkeeping are important.

When to Speak With a Tax Professional

Certain situations require guidance beyond calculators. High income levels, large asset sales, complex investment activity, or multi-year planning needs can introduce rules that are difficult to model accurately. Tax professionals can address individual circumstances, apply detailed regulations, and ensure compliance. Seeking help early can prevent costly mistakes and improve long-term outcomes.